Have you ever felt your stomach turn when the conversation turned to budgeting – or worse yet, more complex topics like investing in the stock market?

I still get this often. Despite working for a fintech, and despite my sixteen years of education, I still don’t feel confident handling my finances – and a quick Google search shows I’m not the only one.

Research suggests that the UK has one of the lowest levels of financial literacy in the world, and the Financial Times reported that Britons between the ages of 16 and 24 are the least likely generation to be financially literate.

Students and young people like me, who are leaving home and becoming financially dependent for the first time, need to know how to budget and save, as well as how to start investing for their future – so where are we failing, and what can fintechs do to help?

But first, is it really that bad?

According to a survey conducted by the Money and Pensions Service in 2019, only 38% of children and young people remember learning about finance management at school, while fewer than half (44%) felt confident about how to manage their money.

It’s clear that financial education in schools and universities is still lacking (despite it being made mandatory in 2014), but research shows that 57% of adults continue to feel overwhelmed or stressed when speaking to financial services providers, or else they struggle to find suitable financial products or services.

Plus, study after study has proven that when it comes to financial wellbeing, women and under-represented groups (such as BAME and LGBTQA+ communities) are the worst affected.

Why does it matter?

On an individual level, poor financial education means less opportunities, freedom and autonomy for the “bottom 98%” (I.e., those of us who aren’t billionaires). It means there is an uneven playing field, and that the financial markets are reserved for only the most affluent.

People with low financial literacy are more likely to become vulnerable due to debt, or fall prey to predatory lenders and fraud. Without financial education, my generation is handicapped from becoming financially secure. Debt and money trouble can also cause or contribute to severe mental health issues, poverty and stress. The list goes on…

On a societal level, it’s also bad for the economy. Studies show that if the UK population was better educated around money, there would be an additional £6.98 billion poured into the economy each year, totalling £202 billion by 2050, and the potential for 123,000 direct jobs – reducing unemployment rates by 8%.

Bridging the gap – a cause for hope

During my placement at Seccl, I’ve been lucky enough to come across a whole range of fintechs in the market trying to further financial education for young people and bridge the investing and advice gaps, some of which we’ve launched or partnered with.

This is not an exhaustive list by any means, but it does give a good picture of how fintechs are responding to this crisis.

-

Financial education for kids: GoHenry

Let’s start off with a bang. Louise Hill, founder of GoHenry, recently shared at the 2022 Innovate Finance Conference that children who receive some form of financial education are 42% more likely to start a new business in adulthood, contributing a potential 6.6 billion to the UK economy every year and saving around £70,000 more towards retirement – a startling statistic.

GoHenry is a financial education and savings app for 6-18-year-olds.

In December 2020, GoHenry reported 1.2 million active customers on the app, and 89% of app users’ parents said they would have made better financial decisions if they had received financial education by the age of 18. Their mission is to “instruct children about money in a way that resembles the world they are growing into.”

-

Educational investment platform: Tillit

Another company taking users behind the smokescreen of jargon and acronyms is Tillit. Their name means “trust” in Swedish, and it’s indicative of what they stand for as a business: clarity, transparency and conviction.

Operating on a Seccl-powered platform, Tillit is a DIY-investing platform offering funds, investment trusts and EFTS across a range of asset classes and investment styles – all while educating users and empowering them to make informed decisions.

-

Saving and pensions: Chip and Penfold/Tumelo

Companies like Chip make automatic saving easy by rounding up your spending and landing you the best rates, while Penfold helps you keep track of your pension (whether you’re employed or self-employed) via a simple app. If you’re interested in where your pension is invested (which everybody should be!), Tumelo gives you the tools to vote on proposals of companies you’re invested in, so you can have your say on defining issues and see the impact.

-

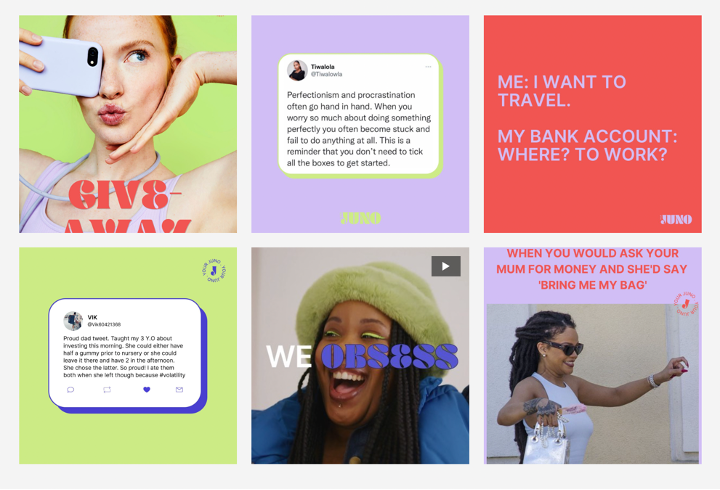

Financial education for minorities: Your Juno

Meanwhile, Your Juno, a start-up founded by sisters Margot and Alexia de Broglie, empowers women and non-binary people to save, budget and invest. Their mission is to make sure “there isn’t a single woman or non-binary person that feels overwhelmed by managing their money.”

Your Juno on Instagram

The company offers in-app courses and free educational videos, as well as business workshops. They have already partnered with Wise, TechSpace, and Circa5000 (another company from the Seccl stable!) in their short tenure, and they recently announced $2.2 million in seed funding.

The future of Your Juno looks promising as they make plans to expand globally, and to extend their offering.

-

Financial coaching: Octopus Moneycoach

Octopus Moneycoach is a new financial coaching service for employers to offer their staff at a greatly reduced cost – you’re also able to sign up as an individual. Users can get one-to-one guidance on budgeting, saving and investing from qualified financial coaches. They also have a series of webinars and helpful resources on their website.

-

Hybrid advice: MoneyMeans

The rapid evolution of technology in this space is also cause for hope, as more advice and investment firms adopt hybrid ways of giving advice and guidance.

Helena Wardle, Chartered Financial Planner at Smith & Wardle, and founder of Money Means

Just recently, at a Seccl offsite event, we heard from Helena Wardle, the founder of upcoming app Money Means, which aims to provide younger generation with different forms of expert financial advice, whether that’s via an app, through text or through TikTok. She argued that to get to the next generation of savers and investors, advice firms need to “go where Gen Z are!”

Embedded investments

Our Fintech Growth Lead, Mary Agbesanwa, on a recent panel on financial inclusion, argued that more non-financial-services companies should be embedding investment platforms into their technology.

“How much easier would investing be, if every time you purchased something from Amazon you could round up your spend with an investment, or if you could send 10p to your investment portfolio every time you used your credit card? There are studies that show this drives consumer engagement and loyalty as well as solving some of the distribution and access challenges with investing.”

A current example of embedded investing in action would be John Lewis partnering with digital wealth manager, Nutmeg, to save into a JISA, a stocks and shares ISA and a General Investment Account. But this is just the beginning…

Millennial and Gen Z consumers are statistically more likely to use embedded finance tools like BNPL (Buy Now, Pay Later) solutions than older generations, and 38% of young people use mobile wallets and digital payment software – so this area is ripe for disruption.

The only way is up: better financial education for all

When it comes to improving financial education for students and young people, there are no shortage of fintechs entering the market with new and innovative propositions.

Having had my ear to the ground as an Intern at Seccl for the past few months, I’m confident that we will see even more innovation in this area over the coming years, and that change will come thick and fast.

However, I think it’s clear that in order improve the financial literacy of the population, we need to start early. Managing my finances as a student would be a lot easier had GoHenry or any one of the other children’s money apps when I was a kid. And now that technology is on our side, we need to make sure everyone has access.

Interested to read more about financial inclusion? Check out Mary Agbesanwa on a UK Fintech panel. If you have any questions or feedback, feel free to get in touch here.