Now that January has rolled around and the dust from Christmas and New Year has settled, it seems like the perfect time to reflect on 2021, examine some of the key trends we’re seeing in wealth management, and discuss what all this might mean for the next few years in our industry.

Before we get stuck in, if you want to hear me talk more about these trends in person, make sure you tune in to my upcoming talk on the future of wealth management. I’ll be discussing the innovations, automations (and, of course, efficiencies) we’re seeing now, and that we’re likely to see in the future.

In particular, I’ll explore the key areas for automation within the advice and investment journey and demonstrate how firms of all sizes can achieve new heights of operational efficiency. You’ll also be able to ask questions about any of these topics, so it’s not to be missed!

You can register your place here.

No time like the present – where are we now?

Here at Seccl, we’re lucky to have a real-time overview of new and emerging trends in the wealth management industry, as well as their impact on the market.

We work with all kinds of firms – new startups, established advice firms, PE-backed advice consolidators, financial coaching platforms, asset managers and crowdfunding platforms to name a few. The truth is that vast amounts of money are being invested into fintech here in the UK at the moment (£1 in every £4 globally). In 2021, there was a whopping £10bn invested in UK fintech – a 300% increase since 2018 (£3bn). What’s more, the number of new businesses launching or enhancing their proposition using our APIs is astonishing.

Having had many conversations with these firms over the past year (both in the UK and overseas), these are some of the key technology trends I’ve observed…

Hyper-customisation

Technology has brought a lot to our lives, but perhaps the biggest impact has been overwhelming choice for the consumer. Just think about how many streaming services there are on your TV; how you can listen to practically any song in the world at any moment and order any kind of food to your door, all from the device in your hand.

In the wealth management space, we’re seeing a shift away from excessive choice and a move towards hyper-customisation. This applies to both the proposition itself, and the investments being offered.

What does this mean exactly? Well, at a proposition level, it’s about designing a service for a specific audience – rather than a generic catch-all one that anyone might use. Historically, financial services has been heavily influenced by a kind of “build a product, try and sell it to anybody” mentality. The result is a huge sales team you can’t afford trying to push a product that most people don’t want.

However, by building a product for a specific audience, your likelihood of referral is much higher, the customer journey is far more optimised, and in turn your customers are likely to be happier because you’re catering to their exact needs, rather than trying to appeal to the masses.

It results in a more engaging proposition, and usually far stronger unit economics, too. In my opinion, virality in financial services won’t be possible if you’re simply selling a product. By selling a community and set of values, you become more of a network than a product. (VCs will flock to any business that can start to illustrate this!)

Here are some examples of hyper-customisation in action…

Daylight is a hyper-customised LGBTQ+ bank using APIs

Daylight is an American LGBTQ+ bank that allows users to change their pronouns easily and use a name other than their registered name. It even provides a “queer-friendly score” for merchants, so consumers can be more mindful about where they spend their money.

Closer to home, businesses like Penfold cater specifically to the self-employed market, and Your Juno is designed to help improve financial education for women, in what is an inherently male dominated domain. Businesses like Wealth8, meanwhile, are aimed solely at the Black and multi-ethnic community.

There’s a reason all this is happening now. With outsourced API-based infrastructure, it’s cheaper, faster and easier than ever before to build a proposition from the ground up. As an organisation, you’re able to give way more units of energy to building your segment – and as your success grows, you can add new services through API (Application Programming Interface) integrations. This covers everything from cloud storage, banking services and of course trading, custody, portfolio management and tax wrappers!

Embedded finance

Years ago, consumers would have to walk into a physical bank to apply for credit. Now, through embedded finance propositions, they can make a purchase and get credit in one place – for example, through Klarna or Afterpay on whichever retail site they’re using.

Simply put, ‘embedded finance’ allows financial services to be made available where and when consumers need them.

Again, it’s made possible through APIs – meaning companies don’t have to build from scratch key financial infrastructure, but instead simply plug into it.

According to a Forbes article published in 2021, embedded finance has an estimated market value of over $138 billion by 2026. So it’s clearly no passing fad.

To provide several examples, Crowdcube recently launched with IPO and listed equities functionality to complement their unquoted early stage offering. And we’ve already seen digital banks launch fully digital investment propositions, such as Chip.

Bumped partnered with Starbucks to reward customers with fractional shares

Going one step further, a US stock rewards company called Bumped recently shared results of a test they ran with Starbucks. Customers who were rewarded fractional shares of stock every time they bought a coffee visited the store 35% more often and spent 53% more every month. These are pretty astonishing early engagement numbers, and an inspiration for all D2C brands to reward customers with fractional equity in an embedded way…

Finally, businesses that aren’t yet regulated can build communities and later embed financial services into their proposition. As Andreessen Horowitz’s Angela Strange once said, "every company will be a fintech.”

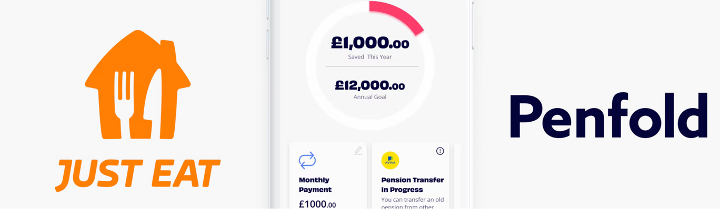

Other case studies include products that support the growing community of gig economy workers – for example pensions and insurance for delivery drivers – many of whom are technically self-employed. Take Penfold, one of our clients, who recently announced a partnership with Just Eat to provide pensions for their drivers.

Penfold now offers pensions for Just Eat drivers

I’ll leave you with perhaps the greatest example of embedded finance in action. Alibaba, the multinational e-commerce and technology company, launched an option for merchants using their eBay-like platform to round up cashflow into money market funds. Within five years, its fund was the biggest in the world at $250bn – astonishing for a company that you previously wouldn’t have said operated within fund management!

Stewardship and impact

Environmental and social concerns are at the heart of investing

Environmental and social concerns have played a huge part in defining the last few years – from Greta Thunberg’s school strike to the Black Lives Matter and Extinction Rebellion movements. Whatever your level of engagement with this kind of activism, it’s become clear that consumers and organisations are voting with their wallets. Increasingly, we’ll see people voting with their investments, too.

In the UK, Tumelo launched to drive ownership and accountability for the retail client by helping them understand where their money goes. We also recently joined forces with CIRCA5000, an investment platform working “to enrich people and the planet”.

From my perspective, when we talk to people launching new D2C investment propositions in the UK, as a default they are almost always thinking about impact. This kind of social and environmental consciousness is no longer nice to have – it’s become essential.

Operating your own adviser platform

In the world of financial advice, there is a continued convergence around themes that are fast becoming necessities in the D2C world: instantaneous investing, entirely paper-free user journeys, open banking availability to name a few – not to mention the use of technology to better segment client bases in accordance with PROD.

What will emerge in 2022 is something the sector hasn’t really witnessed until now – advice firms and consolidators building bespoke platforms using API based technology.

Moving forward, there will simply be no need to hold different clients on lots of different platforms. APIs will allow firms to build their business on truly customisable foundations – not to mention helping them to drive operational efficiency and own all their data in real time.

Building highly customised investment platforms is now commonplace in the D2C space – and I think we’ll see more firms within financial advice and wealth management realise the enormous gains, too.

To sum it up: last thoughts

It’s hardly a coincidence that most of these trends are made possible by reliable, low-cost, cloud-native and API-driven infrastructure – both client and market facing.

Just as the emergence of cloud storage in the early 2000s helped to massively reduce the barriers to building and launching a tech company, so too will they unleash a whole wave of innovation here in the worlds of wealth management, financial advice and investing. Which is just what the customers of the future need.

If you’d like to find out more about what we do here at Seccl, or to chat through any of the themes from the Wealth & Asset Management report, feel free to get in touch – We’re always up for chat.