A few weeks ago, I had the opportunity to chair a Seccl and 11:FS roundtable on embedded investing, bringing together leaders from across banking, fintech and wealth.

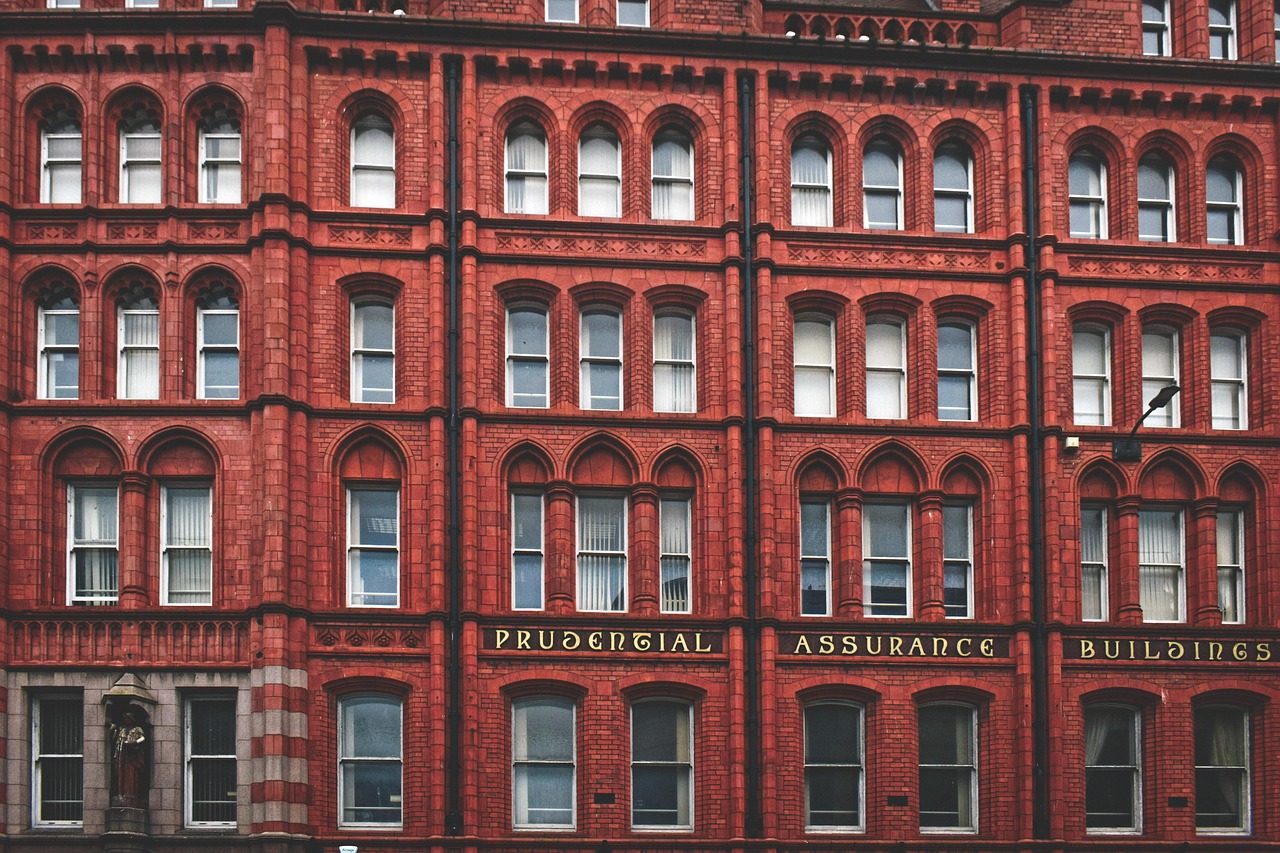

At the start of the session, Benjamin Ensor (Strategy Director at 11:FS) pointed to the old red-brick Prudential building just outside our London offices – a landmark that says more about trust in financial services than most slide decks ever could.

Standing proudly by Holborn circus, it stands as a reminder of a time when “the man from the Pru” was a fixture in millions of households. He wasn’t just selling policies. He brought investing and protection to your doorstep in a way that felt personal, familiar and reassuring.

That framing stayed with me. Because for all the talk of distribution and product experience, the embedded investing opportunity ultimately hinges on something far more fundamental: trust.

Trust is the real distribution advantage

As part of the roundtable, we unpacked the findings from our joint report, Taking Advantage of the Embedded Investing Opportunity. We were joined by leaders from Barclays, Monzo, Tide, Starling Bank and Beanstalk – and while perspectives varied, one theme surfaced repeatedly.

The mechanics of embedded investing matter – infrastructure, integration, user journeys. But the determining factor is far more human: who has earned the right to help someone invest?

The UK has a growing base of new and younger investors. More people are taking their first steps – often through digital platforms – yet confidence still lags and significant sums remain in cash.

Take junior ISAs. By definition, JISAs are long-term vehicles designed to harness compounding over 10–18 years – arguably an ideal use case for investing. And yet a large proportion of JISA subscriptions are still placed into cash accounts rather than invested in the markets.

Encouragingly, the figure is moving in the right direction – 36% in the most recent reported tax year, down from 42% the year prior. But it still points to a persistent instinct to default to cash, even when time horizon is clearly on your side.

For those of us in the investments profession, that’s both understandable and frustrating – understandable because cash feels safe, frustrating because the opportunity cost over 18 years can be significant.

And it underlines the broader point: this isn’t simply an access problem – it’s a trust and confidence problem. Embedded investing has the potential to close that gap, but only if it builds on relationships that already carry credibility.

Context matters more than capability

One of the most energising parts of the discussion was around context. Not every brand with a large user base can – or should – embed investing.

If Uber were to launch an investment proposition tomorrow, it might resonate strongly with drivers who earn their income through the app and already rely on it financially. For riders, whose relationship with Uber is purely transactional, the leap to trusting it with long-term savings would feel far greater.

The difference isn’t product design. It’s proximity – and trust.

That’s why embedded investing is therefore more than a distribution shift. It’s not simply about placing an investment product inside another app. It’s about introducing investing at the right moment, in a familiar environment, where confidence already exists.

Done well, it feels like a natural next step rather than a hard sell.

Simplicity builds confidence

Experience plays a critical role here. If trust gets you through the door, simplicity keeps you moving.

We discussed the importance of progressive disclosure – clear defaults, small first steps and the option to go deeper as confidence grows. Too much information too early can reinforce the perception that investing is complex or reserved for experts.

Embedded investing works best when it mirrors how people already manage money – round-ups, prompts when cash balances build, goal-based framing that connects risk to long-term outcomes rather than short-term volatility.

In that sense, done well it can recreate something of what “the man from the Pru” once provided: guidance at the moment it’s needed, delivered in a context that feels normal.

Targeted support and the advice gap

We also explored targeted support and its potential to reshape how guidance is delivered. There was clear optimism that this direction of travel can help close parts of the advice gap – offering meaningful nudges without requiring full regulated advice at every turn.

But again, trust is decisive. Customers need to believe that prompts are aligned with their interests – and that’s far easier to establish when investment propositions sit within relationships that already deliver value.

An ecosystem built on trust

For many brands, the opportunity will lie in partnership. Investment-as-a-Service models allow customer-facing firms to focus on engagement and experience, while regulated partners manage permissions, infrastructure and operational complexity.

Trust operates at multiple levels – brand, regulatory and technological. Get those layers right and embedded investing becomes scalable as well as compelling. Get them wrong and no amount of clever UX will compensate…

A new default for investing

What struck me most from the session was the clarity of consensus. Embedded investing isn’t about adding another product to an app. It’s about normalising investing – making it a supported, everyday part of financial life for new investors, under-invested savers and future generations.

But the gateway remains trust. The brands that succeed will be those that understand their relationship with customers deeply – and design investment journeys that feel like a continuation of that relationship, not a departure from it.

If you’re exploring how to embed investing within your proposition, start there.

And if you’d like to dive deeper into the data and strategic implications behind this discussion, download our full report, Taking Advantage of the Embedded Investing Opportunity.